During its meeting of April 13, 2022, the Monetary Policy Committee (MPC) of the Centrale Bank van Aruba (CBA) decided to raise the reserve requirement rate from 18.0 percent to 20.0 percent as of May 1st, 2022. This decision was primarily based on the persistent elevated level of excess liquidity at the commercial banks, as well as the continued rise in inflationary pressures.

The following information and analysis were considered in reaching this decision:

International reserves

International reserves, comprising the official reserves of the CBA and foreign exchange reserves held by the commercial banks, strengthened by Afl. 362.2 million. The component official reserves (including revaluation differences of gold and foreign exchange holdings) grew by Afl. 319.7 million on March 25, 2022, compared to end-December 2021. Consequently, on March 25, 2022, the official reserves and the international reserves (including revaluation differences of gold and foreign exchange holdings) stood at Afl. 3,064.6 million and Afl. 3,491.8 million, respectively. For the remainder of 2022, further expansions in international reserves are likely on account of foreign exchange inflows from tourism activities, foreign borrowings, and foreign direct investments.

As a result, international reserves are anticipated to stay well-above the benchmark of 3 months of current account payments (including oil) for the remainder of 2022. Official reserves will also stay within an acceptable range if the IMF ARA metric is applied.

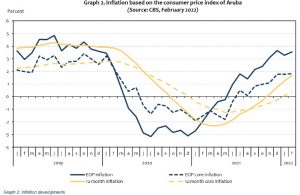

Inflation

In February 2022, the year-over-year CPI rose by 3.5 percent, compared to the corresponding month a year earlier, up from 3.3 percent end-January 2022. This hike was caused mainly by gasoline prices, impacting thereby the ‘transport’ component (+1.5 percentage points contribution). Gains in other components also drove up inflation, i.e., ‘household operation’ (0.3 percentage point contribution), ‘recreation and culture’ (0.3 percentage point contribution), ‘miscellaneous goods and services’ (0.3 percentage point contribution), ‘clothing and footwear’ (0.2 percentage point contribution), ‘restaurant and hotels’ (0.2 percentage point contribution), and ‘housing’ (0.1 percentage point contribution). The 12-month average inflation for February 2022 climbed to 1.7 percent, and is expected to continue to increase throughout 2022. This expectation is based on the rising price level particularly in the United States and Europe, which is the result of (1) the war in Ukraine, and (2) the ongoing logistical problems hampering production and the supply chain. Meanwhile, in February 2022, core inflation reached 1.8 percent on a year-over-year basis and 0.3 percent on 12-month average basis.

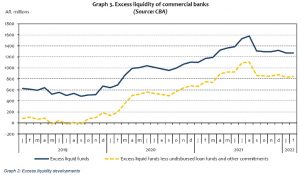

Commercial bank liquidity

Aggregated excess liquidity fell from Afl. 1,320.5 million in December 2021 to Afl. 1,271.0 million in February 2022. This drop in excess liquidity was mainly due to the one percentage point uptick in the reserve requirement on the 1st of January 2022 and, subsequently, another one percentage point increase in the reserve requirement on the 1st of February 2022. Nevertheless, the level of excess liquidity remained significantly above pre-pandemic levels. The elevated level of excess liquidity is the result of the continued subdued credit demand at local commercial banks, in addition to a heightened level of liquid funds held by commercial banks.

Credit developments

In February 2022, total credit of the commercial banks contracted by Afl. 43.6 million or 1.1 percent to Afl. 3,781.3 million, when compared to December 2021. This decline was mostly caused by a downturn in ‘business loans’ (Afl. 31.0 million/2.1 percent), which largely resulted from dwindling term loans with a maturity longer than 2 years (Afl. 34.7 million/4.2 percent) and current account loans (Afl. 12.3 million/8.2 percent). Furthermore, the component ‘other’ put downward pressure on overall credit during the period under review, as it declined by Afl. 14.1 million or 3.3 percent. For the remainder of 2022, credit is expected to stay relatively flat.

Developments in commercial bank deposits

In February 2022, overall deposits stood at a level of Afl. 5,073.4 million, down marginally from Afl. 5,079.0 million registered at December 2021. Time deposits lessened by Afl. 69.7 million compared to December 2021. On the other hand, both demand deposits (Afl. 59.2 million) and savings (Afl. 4.8 million) climbed in February 2022.